The (Hidden) Cost of “Soft Fraud”

When was the last time you told a white lie? To a spouse, to a friend, or maybe a co-worker? Maybe it was to protect their feelings, to prevent them from feeling left out, or to exaggerate your gratitude. While theoretically altruistic in nature, and hypothetically harmless in intent, near-truths have become accepted as the norm.

In the world of insurance, these suggestio falsi can have real financial and even legal consequences; to both you and your carrier.

It is estimated that upwards of 14% of Americans admitted to lying to their car insurer in 2021, a 2x increase year-over-year. Richard Laycock breaks down some interesting rationale for these half-truths, or “soft fraud,” here. The most common reason is to try and get a lower premium. Other reasons include hiding a past accident or ticket or deliberately misrepresenting the vehicle’s use (for example, claiming it’s used for business when it’s really only used for leisure).

Most interesting, in my opinion, is the generational stratification showing how much more younger applicants are lying than their older counterparts. The study found that there is a generational stratification when it comes to lies told to insurers. Baby Boomers were the least likely to lie, with only 8% admitting to doing so. Generation X was next at 11%, followed by Millennials at 15%. The most likely group to lie were those in Generation Z, with 18% of respondents admitting to telling falsehoods to their insurers.

While there’s certainly a correlation v. causation conversation to be had, it’s hard to ignore the factor that the digital age plays in this. Put another way, would it be easier to tell that white-lie face-to-face, or behind a keyboard?

As the P&C insurance world continually trends towards instance issuance, automated claims payouts, and embedded policies, to the benefit of all I may add, I predict we see this soft fraud continue to compound. To that end, I argue that data is the solution. And further, this data should be thought of in two key buckets: the what and the how.

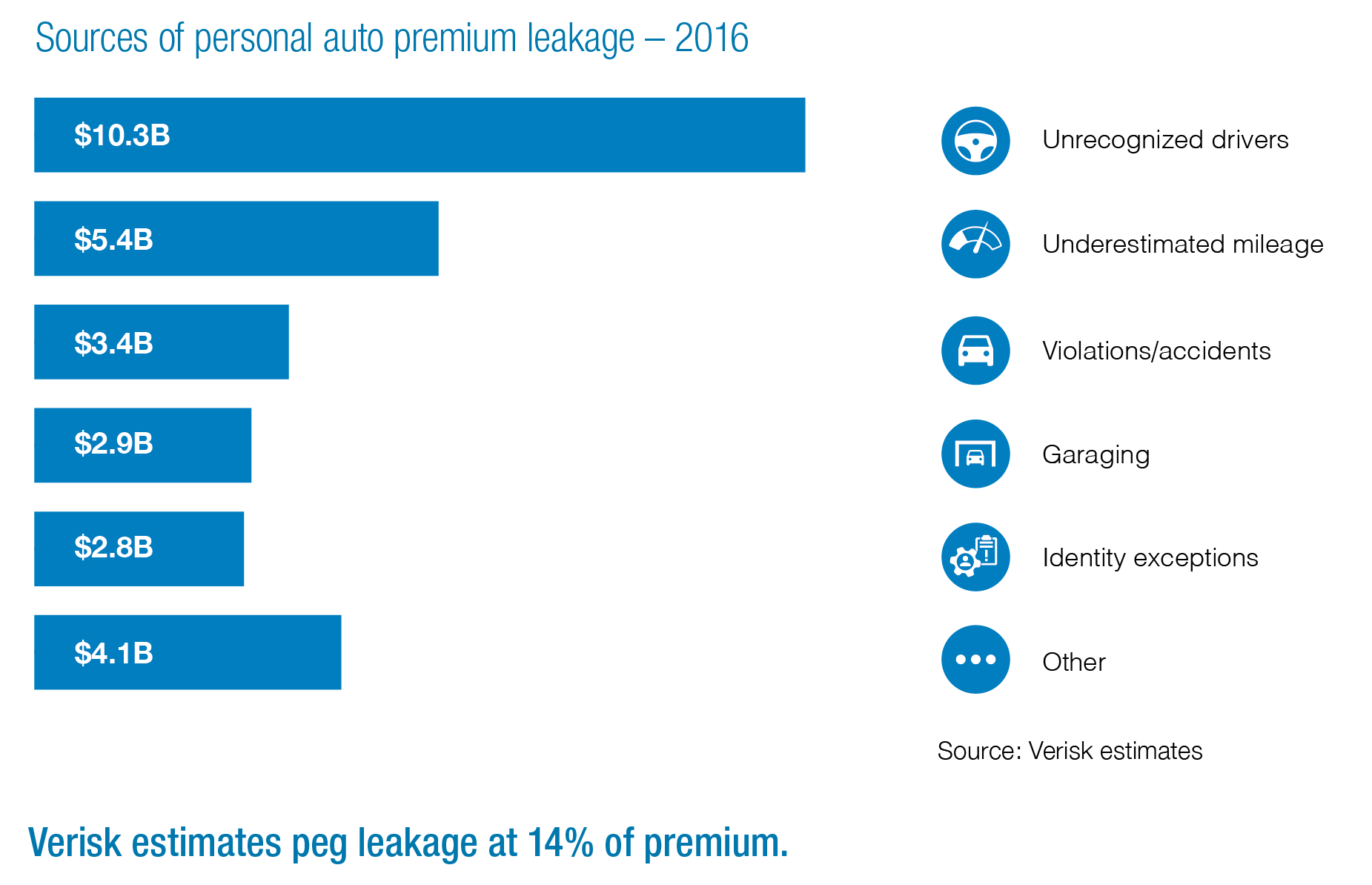

What is the cost of soft fraud in insurance?

According to Verisk estimates, personal lines automobile insurers face at least $29 billion a year in premium leakage—missing or erroneous underwriting information that undermines their rating plans.

How to Reduce Soft Fraud in Insurance Using “What” and “How” Data

“What” Data: Customer Submitted Information

Customer-submitted data can be nearly instantaneously verified by numerous 3rd-party data aggregators: the likes of LexisNexis, Verisk, Experian, MVRs, etc. These data sets are voluminous, and readily accessible through pipelines that are easily configured to your digital streams. Using “what” data can add a level of confidence to your automated workflows, and decrease your overall risk profile.

Pros: vast data sets, nearly-real time, and available from multiple sources

Cons: 3rd party, sometimes stale or inaccurate, and expensive

“How” Data: Digital Behavioral Data

A new dimension of data has been gaining popularity in the world of digital-first: behavioral data. This “how” data is a first-party data set and readily accessible on your consumer and agent-facing applications. Just like your spouse may pick up on some subtle tell of yours when placating an argument, behavioral data empowers carriers to visualize the “digital body language” of consumers to sniff out soft fraud as it happens. By factoring “how” data into automated workflows, carriers can deliver truly personalized user interfaces dynamically to behavioral input e.g. adding reflexive questions to affirm specific information with the ultimate goal being to reduce the cost of soft fraud.

Pros: 1st-party, truly-real time, inexpensive

Cons: non-binary and requires a fully digitized medium

To summarize, carriers today can combat the swelling pattern of soft fraud, by ensembling, multiple data sets together to improve overall loss ratios, without having to degrade their customer experience.

Want to learn more about how some of the largest P&C carriers in the world are leveraging behavioral data to reduce premium leakage and soft fraud? Let’s chat.